Transitioning to a green economy

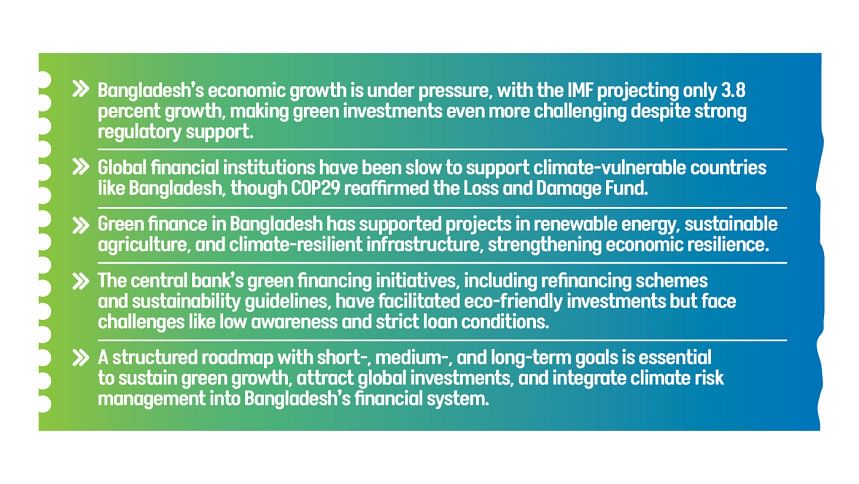

It is perhaps not the best time to discuss Bangladesh's growth story, which is definitely under severe pressure. The latest World Economic Outlook of the IMF projects that Bangladesh's economy may grow at 3.8 percent, the lowest rate in decades. Adding a green prefix may seem even more challenging. Green growth presupposes a huge investment in technologies that may not be forthcoming at this critical juncture for the economy. However, Bangladesh has a long legacy of green growth due to strong regulatory support for financing it. Budgetary support for adaptation and mitigation measures has also been remarkable, despite Bangladesh's perennial record of a low tax-to-GDP ratio. Following the Paris Climate Agreement, Bangladesh has been aligning its fiscal and monetary policies with the goals of sustainable development despite many resource constraints.

However, the global financial sector has been slow to respond to the downside risks of climate change, though it offers the potential to help bridge the financing gap for the adaptation and mitigation strategies needed by climate-vulnerable countries like Bangladesh. Although the recently concluded Conference of the Parties (COP) in Baku did not see the developed world pledge significant additional finance to developing countries, there was no indication of abandoning the deal—thanks to the diplomatic push by environmental activists.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

The developed world promised to maintain the status quo with some marginal additions (not immediate) to the Loss and Damage Fund. Also, at COP29, global leaders agreed to fully operationalise the Fund starting this year. The total pledged fund currently stands at $730 million, which should be increased as climate change continues to create havoc in the developing world. A public policy push is also needed to create a pro-climate environment for private green finance and to attract investment from international financial institutions. In other words, the financial sector must prepare for a green future by enhancing the resilience of banks and financial institutions to both physical and transition risks. Simultaneously, governments must play a significant role in supporting green finance through incentives and adherence to market mechanisms.

Undoubtedly, financing green growth in Bangladesh is crucial, as investing in green growth offers a pathway to sustainable development, environmental preservation, and enhanced resilience against climate-induced adversities. Despite the lower growth prospects in the near future, Bangladesh cannot shy away from its focus on green finance. Green financing supports projects that reduce pollution, promote renewable energy, and encourage sustainable agricultural practices, thereby mitigating environmental degradation. For instance, the adoption of solar irrigation systems reduces reliance on diesel pumps, decreasing greenhouse gas emissions. Investments in green infrastructure, such as flood defences and climate-resilient housing, strengthen the country's ability to withstand natural disasters. This resilience is vital for protecting lives, livelihoods, and economic assets.

The private sector (both non-profit and for-profit) deserves credit for cultivating this culture of resilience in Bangladesh. Green growth also fosters the development of new industries, such as renewable energy and sustainable agriculture, green apparel industries (with 232 LEED-certified green factories, including 92 platinum-rated), and green housing complexes, creating employment opportunities and diversifying the economy. This diversification also reduces economic vulnerability to climate-related shocks.

Bangladesh has undoubtedly made significant strides in promoting green finance. The central bank's latest report indicates that during FY23, banks disbursed Tk 126.41 billion, and non-bank financial institutions (NBFIs) disbursed Tk 23.58 billion in green finance, accounting for 5.84 percent of total term loan disbursements. Additionally, the establishment of the Green Transformation Fund (GTF) has facilitated sustainable export growth as the nation transitions to a greener economy. Notably, this green financing continued even during a clear tightening of credit growth to address high inflation. Despite these efforts, challenges such as limited awareness, inadequate prioritisation of public investment, and weak inter-ministerial coordination persist. Addressing these challenges requires:

1) Implementing robust policies that incentivise green investments and ensure effective environmental governance.

2) Improving inter-ministerial coordination and fostering productive dialogue between the public and private sectors.

3) Investing in skills development to support new engines for green growth and ensure a just transition. Bangladesh has not been shying away from this green policy response. Bangladesh Bank is implementing a refinancing scheme with a fund of Tk 4 billion to support environmentally friendly products, projects, and initiatives. Under this scheme, customers can access loans at an interest rate of up to 3 percent for government-priority sectors like solar irrigation. The loan tenure ranges from 3 to 10 years, facilitating long-term investments in sustainable technologies. Support from banks and financial institutions has led to the installation of numerous solar-powered irrigation pumps across the country, particularly in deltaic char lands. These pumps provide reliable and cost-effective irrigation solutions for farmers, reducing operational costs and minimising environmental pollution associated with diesel pumps. Additionally, rooftop solar energy production and distribution have been flourishing following the introduction of the net-metering policy, which could be further improved with additional incentives for green energy producers.

Bangladesh Bank's refinancing schemes have facilitated investments in renewable energy, energy-efficient technologies, and sustainable industrial practices, contributing to a reduction in greenhouse gas emissions and environmental pollution. Funds like the GTF have enabled export-oriented sectors, such as textiles and leather, to adopt eco-friendly technologies, enhancing their competitiveness in global markets that increasingly value sustainability. The availability of refinancing has supported the development of infrastructure and capacity necessary for climate resilience, including waste management systems and energy-efficient machinery. However, despite the availability of funds, challenges remain. For example, utilisation rates have been suboptimal due to factors such as a lack of awareness, stringent loan conditions, and limited technical expertise among potential borrowers. Increasing awareness and understanding of sustainability issues among entrepreneurs and financial institutions is crucial to maximising their impact.

Bangladesh Bank recently issued a comprehensive guideline titled "Guideline on Sustainability and Climate-related Financial Disclosure for Banks and Finance Companies," effective from December 26, 2023. This initiative mandates that all scheduled banks and financial institutions in Bangladesh disclose their sustainability and climate-related financial information, including their carbon footprint. The key aspects of the guideline include the disclosure of information about sustainability and climate risks, including climate footprints and opportunities, in line with International Reporting Standards (IFRS S1 and S2). Additionally, a limited supervisory report is required by December 2024, limited disclosures must be included in annual reports in 2025 and 2026, and full disclosures must be made by the end of 2027. Sustainability and climate-related disclosures must be made semi-annually. This move aligns Bangladesh's financial sector with global standards, supporting the transition to a sustainable economy and aiding stakeholders in making informed decisions regarding resource allocation.

The pioneering role of Bangladesh Bank has provided a strong foundation for the proliferation of green finance in the country (see UNEP's Inquiry on Designing Sustainable Finance and its subsequent case studies). Banks and NBFIs in the country have been commendably responsive to these pioneering policy initiatives.

As green finance activities in the country mature beyond their early stages, stakeholders must focus on emerging challenges to bolster green growth. Bangladesh must develop its own tailored solutions, particularly given its resource constraints. Fossil fuel-exporting countries can afford to leverage revenues from fuel exports and public savings to facilitate climate investment. Wealthier economies that rely on fossil fuel imports have the option to develop their capital markets to bolster green investment capabilities. However, neither of these options suits Bangladesh. Excessive debt issuance could crowd out private investment in Bangladesh. Instead, the country should focus on mitigating risks within its financial system, thereby creating a more conducive environment for green growth.

Policymakers and stakeholders must develop a green finance roadmap with short-term, medium-term, and long-term milestones. In the short term, policymakers should prioritise a better understanding and measurement of climate-related risks. This includes implementing methodologies for quantifying and reporting such risks, promoting their transparent disclosure by financial institutions, and strengthening frameworks for forecasting and analysis.

Over the medium term, they can support green finance through incentives and market mechanisms, phasing out energy subsidies, and introducing new tools and markets (such as carbon pricing frameworks) to stimulate investment in green technologies. In the long term, significant collaboration is needed between the public and private sectors, involving international financial institutions, multilateral development banks, sovereign wealth funds, and state-owned entities, to bridge the financing gap for climate investment needs. To achieve this, generating and managing well-planned data on green finance—aligned with international standards—must be prioritised to attract global investment in Bangladesh's thriving green economy.

Comments